Learn how to identify and fix 5 common money mistakes that could be costing you thousands annually.

Are you making common money mistakes without realizing it? Financial blunders can cost you thousands of dollars and lead to unnecessary financial stress. According to a survey by Capital One and The Decision Lab[1], 77% of Americans report feeling anxious about their financial situation.

The good news? Most money mistakes are easy to fix once you identify them. In this guide, we’ll reveal the 5 most common money mistakes people make and provide expert strategies to help you avoid them and improve your financial health.

Money Mistake #1: Living Beyond Your Means

With the rise of social media platforms, like Instagram, there’s never been more pressure to appear wealthier than you really are, particularly for younger Americans. Research shows that social media can significantly impact spending behaviors and financial wellbeing among younger generations.

And unfortunately, many millennials are willing to overspend to keep up appearances, whether it’s dining at expensive restaurants, buying designer items, or taking lavish vacations.

Living beyond your means like this can cause a massive strain on your budget and hurt your savings. And if you’re using credit to keep up appearances, you could also be doing some damage to your credit score.

How can I fix it?

Rather than try to follow the spending habits of others, take the time to reevaluate your financial situation. Although there’s nothing wrong with indulging every now and then, it’s important to make sure it fits well into your budget and won’t impact your financial goals.

If you are having trouble with overspending, it might be worth opening a ‘fun account’, so you can indulge without hurting your budget. This is an account that is allocated for everything from nights out to online shopping to travel.

Money Mistake #2: Having No Financial Plan

Whether you’re a pro or novice with managing your money, having a financial plan is essential. Setting financial goals or creating a financial plan is important for maintaining positive financial habits, as it gives you something to work toward and teaches you discipline.

For example, if one of your financial goals is to save for a home down payment or to purchase a new car, you’re more inclined to hold yourself accountable to reach your goal.

How can I fix it?

Spend some time thinking about goals you would like to achieve, big and small. Some common examples of financial goals are to save for an emergency account, pay off debt or start your own business.

Once you’ve got your goals written down, your next step is to create a plan of how you intend to reach this goal. This might look like contributing more to your savings every month or making additional repayments to pay down your debt.

If you’re stumped and are in need of financial inspiration, our Guide to Personal Financial Goals can help point you in the right direction.

Money Mistake #3: Treating Credit As Cash

Some of the most common reasons Americans own credit cards are for emergencies, to earn rewards points or to access other shopping benefits. But because these products can be used just about anywhere, many Americans tend to go overboard with their spending and treat their credit cards like regular cash.

The trouble with doing this is as you start to accrue a hefty balance, your interest bill also begins to climb. And if you’re struggling to get on top of your balance or miss monthly payments, not only might it take years to pay off your debt, credit health might also take a hit.

How can I fix it?

Make getting debt-free your top financial priority and pay more than the monthly minimum repayment. Give yourself a debt-free deadline and create a repayment plan to figure out how much you can afford to pay back every month. This might mean having to cut back in certain areas or finding ways to funnel extra cash toward your debt.

Check out our credit card blog for more details.

It’s also important during this time to learn how to manage your finances without a credit card and establish positive financial habits, like regularly saving and sticking to your budget.

Money Mistake #4: Not Investing

While regularly topping up your savings account can give your financial security, there are other ways to grow your savings, like share trading.

According to a 2021 report by Gallup[2], just over half (56%) of Americans own stocks. Investing offers potential benefits including long-term returns and the ability to continue earning income in retirement.

How can I fix it?

As investing and share trading has gained some traction over the past few years, there are a variety of resources and tools available to help you understand the stock market.

A good place to start might be a micro-investing platform, as they allow you to start investing without a massive initial deposit. They’re also an easy way to understand how the stock market works and gives you the space to play around with different shares.

Of course, there are other investment options such as investment properties, investment bonds, term deposits or even peer-to-peer lending, so be sure to do your homework and choose the option that works best for your financial goals.

Money Mistake #5: Not Using Any Money Apps

Between online banking to contactless payments, personal finance has taken a big digital turn, which is why savvy Americans are opting to manage their finances with the help of apps. Despite the widespread availability of financial management tools, many smartphone users still don’t take advantage of budgeting apps.

If you haven’t jumped on the bandwagon yet, you might be missing out on some priceless perks, as these apps often come with features like spending trackers or payment reminders.

How can I fix it?

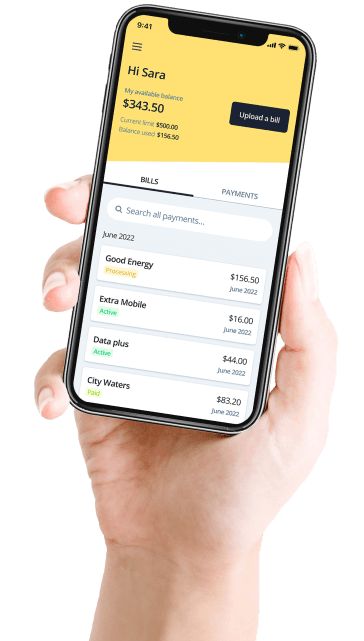

Do some research around the type of apps around to find the one that might work best for your lifestyle and your financial goals. There are a variety of apps around, from those that track your spending, help you pay off debt or even pay and manage your bills, like Deferit.

Deferit is a budgeting app that splits your bills into 4 installments with no interest. Once you upload a photo of your bill, Deferit will pay the biller upfront, meanwhile, you pay your bill back over 4 payments over time.

You can use the platform to pay just about any bill, from your energy bills to medical or dental expenses. Get started with Deferit to take control of your bill payments today.

Want more tips and tricks about effective money management? Check out the rest of our blog! We cover a range of topics from setting financial goals to guides on understanding your credit score.