Discover the key differences between debt consolidation and debt management programs. Learn which debt solution works best for your financial situation and explore alternatives to get debt-free faster.

Understanding the difference between debt consolidation and debt management is crucial for choosing the right debt relief strategy. According to Experian’s 2019 State of Credit report[1], the average American carried $90,460 in debt, including credit cards, personal loans, mortgages, and student debt.

Whether you’re juggling multiple debts or struggling with everyday bills, finding the right debt solution can save you thousands in interest and help you become debt-free faster.

Debt consolidation combines multiple debts into a single loan with one monthly payment, often at a lower interest rate.

Debt management programs, on the other hand, work with credit counseling agencies to create structured repayment plans and negotiate with creditors on your behalf. Each approach has distinct advantages depending on your financial situation.

This comprehensive guide explains the key differences between debt consolidation and debt management programs, when to use each strategy, and alternative solutions for managing bills and expenses - helping you make an informed decision about your path to financial freedom.

Debt Management vs Debt Consolidation

Understanding debt consolidation vs debt management is the first step to eliminating your debt effectively. While both debt consolidation and debt management programs can help you become debt-free, they work in fundamentally different ways. Debt consolidation combines multiple debts into a single loan, while debt management programs work with credit counseling agencies to create structured repayment plans. Choosing between debt consolidation vs debt management depends on your specific debt situation, credit score, and financial goals.

Finding the perfect debt solution will be different for everyone, as no one’s financial circumstance is the same.

There are many methods that can help reduce your debt levels, like debt management, debt consolidation and other alternative tools that improve your overall financial management.

The option you choose will depend on the type of debt you are looking to clear. For instance, if you have multiple debts, such as a credit card or car loan, you might want to think about debt consolidation.

On the other hand, if you are struggling with outstanding payments to billers or credit providers, a debt management program could help you get things back on track. People often turn to solutions like these if their debt has become overwhelming and they can no longer manage it themselves.

And thanks to the rise of various fintechs and digital tools, consumers can take care of their debt from the comfort of their own home. These apps and resources traditionally provide consumers with the flexibility to pay down debt on their own terms.

What is Debt Management?

Debt management or debt agreement programs are a great option for those who need help getting on top of their debt.

These programs are provided by a credit counseling agency who create a repayment plan to clear your debt. They do this by reviewing your current financial situation, assessing how much you could realistically pay back every month.

Once your plan is ready and you understand its conditions, your financial counsellor will then work with you to ensure you make your repayments each month. In some cases, your assigned credit counsellor may even reach out to your credit providers to negotiate a lower interest rate.

You might consider opting for a debt management program if you are struggling to take care of the debt yourself.

What is Debt Consolidation?

Debt consolidation is a common way to refinance your debt. It’s a process that involves taking out a personal loan to roll multiple debts into one monthly payment. The benefit to a debt consolidation loan is that you’ll only have one interest rate and one monthly payment, instead of trying to pay off multiple types of debt with varying interest rates.

Interest rates for debt consolidation loans also tend to be lower than your standard credit card rate or personal loan, helping you trim your interest bill over the long term.

On the other hand, if you only have a singular credit card with a large balance, you might want to consider a balance transfer credit card. This is a type of credit card that features a 0% interest rate for a fixed period before reverting back to a set interest rate.

The main benefit of a balance transfer card is you’ll be able to pay your debt back interest-free. Depending on the amount of debt you’re looking to pay off, interest free periods on balance transfer cards range from 6 to 24 months.

Just keep in mind you will need to ensure you have paid your debt back in full before the interest free period ends, otherwise, you could be staring down the barrel of a high revert rate.

Debt Consolidation Alternatives

For some of us, debt goes beyond credit and can be as simple as a couple of unpaid bills. Nonetheless, defaulting on your bills means late fees and maybe other charges, which add up over time.

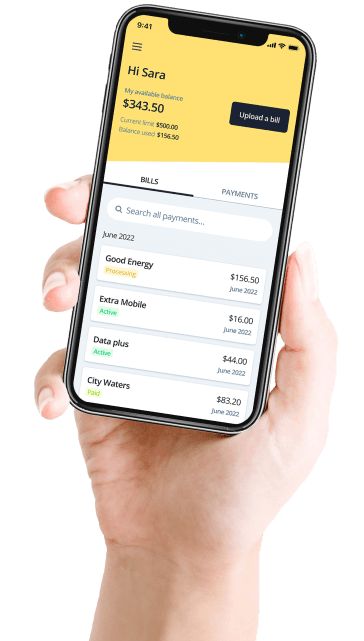

Budgeting apps, like Deferit, can help customers avoid interest on their bills. Deferit allows customers to upload a photo of their bill and pay it over fortnightly installments, meanwhile, the platform pays the bill upfront on the customer’s behalf.

The platform also charges no interest, so customers won’t have to worry about throwing themselves further into debt.

People often consider alternatives like these when they are looking for a debt solution that is flexible to their lifestyle. But like any financial product, it’s best to read through the terms and conditions of the service to ensure it is the right fit for you.

Want to find out if Deferit is the right debt solution for you? Get started with Deferit today to take control of your bill payments!