Master your personal financial goals with proven strategies for short-term and long-term success. Learn how to set achievable financial goals, pay off debt, build emergency savings, and create lasting wealth.

Setting personal financial goals is essential for building wealth and achieving financial freedom, yet most people struggle with where to begin. Whether you want to pay off credit card debt, build an emergency fund, or save for retirement, having clear financial goals provides direction and motivation for your money decisions.

Personal financial goals come in two categories: short-term goals (achievable within 6 months to 3 years) and long-term goals (requiring 3 to 5+ years). Having both types is crucial - short-term goals provide quick wins that keep you motivated, while long-term goals build lasting financial security. Most importantly, financial goals hold you accountable and prevent impulsive money decisions that derail your progress.

The biggest challenge isn’t reaching your financial goals - it’s setting them in the first place. This comprehensive guide reveals proven short-term and long-term financial goals you can start working toward today, plus actionable strategies to ensure you achieve them all and transform your financial future.

Short Term Financial Goal Examples

Setting short term financial goals provides quick wins that build momentum toward long-term financial success. These goals typically take 6 months to 3 years to achieve and focus on immediate financial needs like paying off debt, building emergency savings, or saving for specific purchases. Let’s explore the most effective short-term financial goals you can start working toward today.

Pay Down Credit Card Balances

For many households, credit card debt has almost become a regular part of everyday life. According to financial data company ValuePenguin[1], almost half (45.4%) of American families have some sort of credit card debt, while the average household has a credit card debt balance of $6,270.

Clearing your credit card debt once and for all can give your family more financial freedom, as you’ll be able to focus on building your long-term wealth. There are many ways to pay down credit card debt, such as paying more than minimum monthly repayment or funnelling any extra cash left in your budget toward your debt. But if you’re prepared to aggressively pay down your debt within a small time frame, a balance transfer credit card can help you save on costs and get you debt-free.

A balance transfer credit card is a card that features a 0% interest rate for a fixed amount of time, ranging from six months to as long as three years. This means you can pay back your debt without accumulating any more interest. Just keep in mind that once the fixed period ends, the card will then revert back to an interest rate which can be on the higher side, so you’ll need to ensure you can pay back the full amount before then.

Consolidate and Refinance Debts

From the car loan you took out in your twenties to that last remaining bit of your credit card balance, personal debt can stunt your financial growth. Take it on once and for all by setting up a payment plan that will get you debt-free.

If you have multiple debts that need to be taken care of, consider a debt consolidation loan. This is a type of personal loan that combines different types of debt into one monthly payment.

The benefit of a debt consolidation loan is that you’ll no longer have to worry about multiple interest rates and repayments. These kinds of loans also tend to have lower interest rates than credit cards, helping you save on interest in the long run.

Having a clean slate financially will not only give you the freedom to focus on growing your wealth, but you’ll also be saving a bundle in interest and fees.

A Short Term Savings Goal

In addition to your regular savings account, you should consider setting up an emergency savings account. As the name suggests, this is an account that should only be accessed during unforeseen circumstances, like a sudden vet bill, an urgent car repair or even an unexpected kitchen renovation.

The general rule of thumb is that an emergency savings account should be at least three months worth of living expenses. Depending on your circumstances, aim to save more or less than this amount.

Other short term savings goals you may need to start thinking about are any holidays or travel plans you have coming up. The earlier you start putting money away for these events, the less you will need to rely on credit. If you’ve already started saving for these, set up a separate savings account rather than depositing the money into your regular savings account. Doing this will not only give you a clear overview of how you’re tracking, but will make it difficult to spend the money.

Long Term Financial Goal Examples

Long term financial goals are ones that can take years to reach, as they typically require a larger financial investment. Some common examples of long term financial goals are securing a comfortable retirement, creating a passive income or starting a business.

Paying Off Your Mortgage

Owning your own home is a dream shared by many Americans, but unfortunately, sometimes that dream means having to pay off a mortgage over thirty years. Although a mortgage is considered a positive type of debt, as your home will be used to build wealth, it doesn’t mean you have to take the full thirty years to pay back your mortgage. In fact, with the help of a few strategies, you could shave years off your mortgage.

One option might be to split your monthly mortgage repayments in half and make bi-weekly payments. Depending on your interest rate, this could take between four to six years off your mortgage. It might also make these payments easier to manage and squeeze into your budget. However it’s important to note that not all financial institutions allow bi-weekly payments, so get in contact with the lender to see if this is possible for you.

Another way to not only pay off your mortgage faster, but save on interest, is to refinance your loan. This is an especially great idea to do if it’s been a while since you compared your mortgage against other offers on the market, as you could be missing out on a better deal. While it’s important to compare interest rates, it’s also worth looking into any features that come with the loan, like the ability to make extra repayments for free, which can also help you pay back the loan sooner.

A final strategy is to budget for an extra repayment every year. You can do this by setting aside some extra cash every month or by using your tax refund or any monetary bonus you receive during the year.

Plan and Save for Retirement

Did you know that according to a 2019 survey from Bankrate[2], more than half of Americans are behind in saving for their retirement? If this sounds like you, it might be time you got on top of your retirement savings to safeguard the lifestyle you want to have when you’re older.

Although retirement feels like a lifetime away, the earlier you make a plan for ‘future you’, the better off financially you will be. In addition to your 401k, it might also be a good idea to start building your own retirement fund. Doing this can ensure you retire comfortably and are able to maintain your current lifestyle.

Calculate how much you can afford to contribute to your retirement fund, whether that’s on a monthly or yearly basis, and start making regular contributions. Many financial experts recommend having at least 80% of your final annual income amount. For instance, if you retire with an annual income of $100,000, you’ll need $80,000 per year to live comfortably.

Alternatively, Fidelity Investments[3] suggests following a benchmark based on a multiple of your annual income and your age. For example, at 30, they recommend having one times your annual salary in retirement, which then jumps to four times by age 50.

Long Term Savings Goals

When we talk about long term savings goals, ‘passive income’ is a term that tends to surface. Passive income refers to the idea that a person receives a regular income without the need for intense labour - receiving a rental income through an investment property is one example. However, if you plan to live in the property you plan to purchase, share trading is another common way to generate passive income.

Share trading allows you to purchase and receive dividends with little to no effort at all. As you begin to diversify your portfolio, a passive income stream will form over time. Just keep in mind that share trading is meant to be practiced for the long haul, meaning you need to be comfortable with parting ways with the money you invest for a long time.

Another way to generate income for yourself is to start a small business. Depending on what kind of business you would like to kickstart, going online could be the best way to do it, as you’ll have access to a wider customer base. Starting a business involves some investment on your part, so be sure your budget and savings can withstand this.

Similarly, picking up a side hustle has also become a popular way to boost your income. There are a variety of options available, from dog walking to renting your wardrobe to content freelancing. Aside from the extra bit of cash, another benefit of side hustles is the flexibility since you can choose your hours and set your own rates.

If you’re a parent, setting up a college fund for your children might be another goal to consider. This is an expense that often gets pushed aside for most parents, as other costs can easily take priority. While it’s best to start from when your child is born, any kind of contribution you make now can help your child from having to take out a massive student loan.

If you are looking for some guidance in terms of how you should be saving, Fidelity Investments recommends the ‘2k rule’[4]. This involves multiplying your child’s age by $2,000 for the amount you should have in savings by that age. For example, if your child is four years old, their college fund ideally should be sitting at $8,000.

Create a Budget to Reach Your Goals

Once you’ve got your financial goals set, the next step is to create a strategy of how you plan to achieve them. A good place to start is by revisiting or setting up your first budget. Having a tight budget gives you an idea of where your money is going every month and provides an insight into areas where you can reduce costs to boost your savings.

If it’s your first time mapping out a budget, a good place to start is jotting down your annual income to note the amount of money deposited into your bank account every month. From there, you can run through your bank statements and list all the monthly essential expenses you have, such as your rent or mortgage repayments, utility bills, subscriptions and groceries. You’ll also need to deduct costs such as taxes and your 401ks.

The number you’re left with is now your disposable income and is what you’ll have to spend throughout the month as well as contribute to your financial goals. When deciding how much you’ll be able to put toward your financial goals, it’s important to be realistic and set aside some ‘fun money’ for nights out, shopping and other kinds of discretionary spending, so you’re not tempted to dip into your savings and hurt your financial goals.

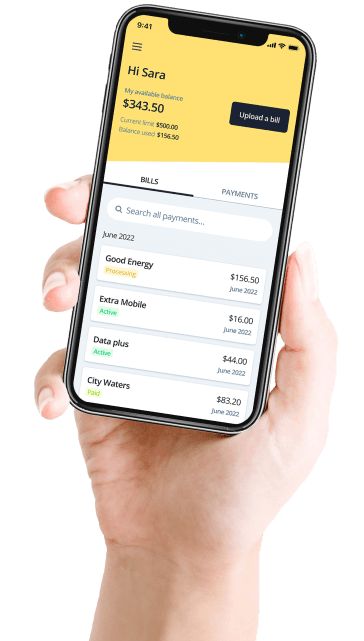

When getting on your feet financially, managing your money can be a little overwhelming. But with the help of innovative budgeting tools, you can stay in control of your cash flow and nail your financial goals.

For instance, Deferit is a budgeting app that helps you stay ahead with your bills. Deferit pays your bills upfront and on time, meanwhile, you pay it back over 4 fortnightly installments. Having every bill paid on time helps you avoid being stung with bill payment penalties. And speaking of fees, Deferit is a 100% interest-free service, making it a cost-effective tool to have in your repertoire.

Want to learn more about how Deferit can improve your financial management skills? Get started with Deferit today to take control of your bill payments and work toward your financial goals!

References

- ValuePenguin. “Average Credit Card Debt in America: 2021 Statistics.” LendingTree. 2021.

- Bankrate. “Financial Security Index Survey - November 2019.” More than half of Americans are behind on retirement savings. Bankrate. November 2019.

- Fidelity Investments. “How much do I need to retire?” Retirement savings guidelines by age. Fidelity. 2019.

- Fidelity Investments. “New Fidelity Analysis Highlights the Financial Burden Facing Parents.” Announcing the “2k rule” for college savings. Business Wire. April 2017.