Expert guide to managing financial stress with practical budgeting strategies, debt management tips, and professional resources for financial wellbeing.

Learning how to manage financial stress is essential for both your mental and financial wellbeing. Financial stress has reached all-time highs, affecting millions of Americans who’ve faced reduced working hours, job loss, and economic uncertainty.

According to a Capital One CreditWise survey[1], a concerning 73% of Americans ranked their finances as the biggest stressor in their life. Ongoing financial stress like this can also negatively impact a person’s mental health, especially if there’s a lack of resources and tools available.

This comprehensive guide will show you practical ways to manage financial stress through budgeting strategies, debt management, emergency planning, and professional resources to help you regain control of your finances.

What is financial stress?

According to University of Wyoming Extension[2], financial stress is defined as ‘a condition that is the result of financial and/or economic events that create anxiety, worry, or a sense of scarcity, and is accompanied by a physiological stress response’.

Some people who have financial stress might experience feelings of shame and anxiety when they think about money. Other common behaviors are canceling social plans to avoid seeing friends and family, recurring feelings of irritability and hopelessness.

Financial stress can be brought about by sudden unemployment, not having enough money to pay for groceries or other necessities or being forced to drain your savings or relying on credit to deal with an emergency. Understanding common money mistakes can help you avoid situations that lead to financial stress.

Budget tips to ease financial stress

Whether you’re planning ahead to avoid financial stress or want to take small steps to improve your current financial health, having the right tools and tips are essential. To save you the trouble from researching the best ways to get back on track, we’ve jotted down our five favorite tips to help you start saving and better manage your budget. For families dealing with financial pressure, check out our money saving tips for families with strategies tailored to household budgets.

Create a monthly budget

If you think your spending has contributed toward your financial stress, it might be time to go back to the basics with a budget.

A budget provides an insight into your cash flow, detailing where your money goes every month. Comb through your most recent bank statements to find out exactly how much you’re spending across various categories, like your essentials and lifestyle.

Once you’ve got these figures down, take notes on where you can afford to cut back on your spending.

For instance, if you enjoy going for meals with friends or frequently head to the shop for some retail therapy, try to make these events a special outing that only happen once or twice a month. Learning how to save money and spend less can significantly reduce financial pressure.

If it’s your first time creating a budget, check out our How to Budget and Save Money blog! It provides detailed steps on how you can draft the perfect budget as well as tips on how you can improve your spending habits.

Prioritize getting debt free

One of the biggest contributors to financial stress is personal debt. This might be a personal loan you took out years ago, credit card debt you can’t seem to get on top of or unpaid bills.

Get serious about paying off your debt by creating a debt repayment plan. To do this you will need to find the balance between knowing how much you afford to put toward your debt every month and the date of when you would like to be debt free.

One effective way to pay down debt is the snowball method, where you pay back your smallest debt balance first, while making the minimum repayments on the larger ones. Once the smaller debt is paid off, you then move onto the larger balance. Having this kind of momentum behind you will keep you motivated to keep going, which will get you debt free in no time!

However, if you’re someone with multiple debts, you might want to consider a different tactic, like debt consolidation. Debt consolidation is a type of personal loan that rolls multiple debts into one monthly payment. Not only does this help you better manage your debt repayments, but you’ll also save a bundle in interest.

If you’d like to learn more about debt consolidation and other debt management strategies, check out our Debt Consolidation vs Debt Management blog.

Save money on utilities

A lot of the time, the simplest way to get ahead financially is to revisit your expenses, as there may be areas where you can reduce costs. For instance, electric bills tend to be one of the highest expenses for a household, after rent or mortgage repayments.

Compare your energy plan against current deals on the market to see if you could be on a cheaper plan. If you do come across a better value offer, making the switch could save you hundreds of dollars annually.

Lowering your electricity usage is another way to cut costs. This could be anywhere from switching appliances off at the powerpoint to only running full loads of laundry rather than smaller, frequent cycles. There are also a range of devices you can invest in that are designed to help your home become energy efficient and lower your annual bill.

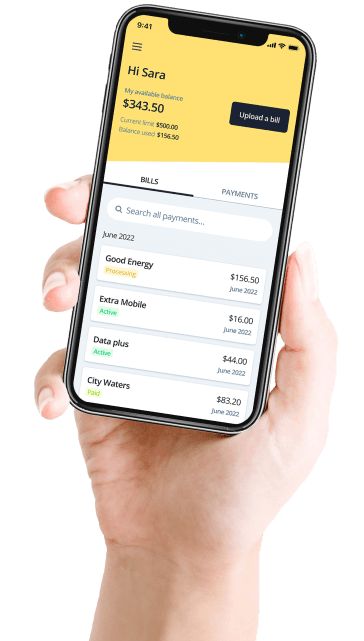

Getting smarter with the way you pay your bills by using services like Deferit can also help you save on late payment fees.

If you receive an unexpectedly high energy bill that’s tough to fit into your budget, services like Deferit can split the cost into 4 installments, making them easier to stay on top of. Deferit also charges no interest, so it takes the stress away if you ever need to change your payment date to suit your lifestyle. Get started with Deferit to take control of your bill payments.

Plan for unexpected expenses

If the last two years is anything to go by, it’s that you never know what’s waiting around the corner. The good news is, no matter what life throws at you, there is a way to ensure you’re prepared for the worst.

While you might already have your standard savings account, it’s recommended to also have a dedicated savings account for emergencies. This is to prevent you from having to take money from your hard earned savings, which then slows you down from hitting your financial goals.

According to a Bankrate survey[3], 56% of Americans confessed they wouldn’t be able to cover a $1,000 emergency expense. If this sounds like you, it might be worth making your emergency savings a top priority. You can also explore ways to get help paying bills during financial emergencies.

An emergency fund looks different for everyone, so it’s up to you to determine how much you would need to get yourself out of a sticky situation, although a general recommendation is to have at least three months of living expenses stashed away. Some common emergencies people tend to plan for include sudden unemployment, unexpected medical or veterinary bills or an urgent repair.

Ask for help

If things seem beyond your control and you’re finding it difficult to get back on your feet, there are professionals who can help. In the US, there are free financial counselling services available, which can help you on a range of financial matters, like debt and renegotiating payments with various providers and billers.

Financial counsellors analyze your financial situation, like your income, assets and debts and then come up with a plan and provide advice on how to improve your financial situation.

They may also reach out to various providers to give you some breathing room. For instance, if you are struggling with debt, your financial counselor may contact your credit provider to discuss waiving certain fees or to construct a personalized payment plan. The Financial Counseling Association of America[4] (FCAA) is a non-profit organization with accredited members who offer debt management plans, student loan support and housing assistance.

If you’d like to learn more about how you can improve your financial health, check out the Deferit blog!

References

- Capital One. “Survey Reveals Tension Between Financial Stress and Optimistic Financial Outlook Among U.S. Consumers - CreditWise® from Capital One® Survey.” PR Newswire. October 2019.

- University of Wyoming Extension. “Financial Stress and Your Health.” Mary M. Martin, Extension Educator. September 2021.

- CNBC. “56% of Americans Can’t Cover a $1,000 Emergency Expense With Savings - Bankrate Survey.” CNBC. January 2022.

- Financial Counseling Association of America. “Professional Financial Counseling Services and Debt Management Plans.” FCAA.