Your credit score impacts major financial decisions from loans to credit cards. This comprehensive guide explains credit scores, FICO scores, and proven strategies to improve your creditworthiness.

Understanding your credit score is essential for financial success. Whether you’re applying for a mortgage, car loan, or credit card, your credit score directly impacts your approval odds and interest rates. A strong credit score can save you thousands of dollars over your lifetime.

Your credit score is a three-digit number between 300 and 850 that represents your creditworthiness to lenders. This comprehensive guide explains what credit scores are, how they’re calculated, the difference between FICO and VantageScore, and proven strategies to improve your score - helping you make informed financial decisions and access better credit opportunities.

What are Credit Scores?

A credit score is a number between 300 and 850[1], which tells a person or financial institution how well you manage money. Your credit score number is based on parts of your financial history, like whether you pay your bills on time, the amount of personal debt you currently have and if you’ve ever been rejected on a credit application.

Credit scores are broken up into five categories, where the higher your score, the more financially attractive you appear:

| Credit Rating | Score Range | What It Means |

|---|---|---|

| Excellent | 800 - 850 | Best rates and terms available |

| Very Good | 740 - 799 | Above-average creditworthiness |

| Good | 670 - 739 | Near or slightly above average |

| Fair | 580 - 669 | Below average, higher rates |

| Very Poor | Below 580 | Difficulty obtaining credit |

What are Credit Reports?

In addition to having a credit score, every person over the age of eighteen will also have a credit report. Your credit report is a total record of your past debts, credit applications, repaid or unrepaid loans within the last five years. More specifically, they detail:

- The date you opened an account, how long you’ve had them and their types

- The credit providers or lenders you’ve enquired with in the past

- Any overdue or unpaid debts

- Your current credit limit

A lender or financial institution can access this information if you ever apply for credit, like a credit card or home loan. They do this to help them assess your creditworthiness and the likelihood of you defaulting on repayments.

Credit Scores vs FICO vs VantageScore

Assessing a person’s creditworthiness is done using various score modeling techniques. In addition to ‘credit scores’ the results may also be referred to as FICO scores or VantageScores, but these terms are also often used interchangeably.

The system to determine a FICO score was developed in 1989 where the company uses proprietary systems to produce scores.

FICO scores generally range between 300 to 850[1], where scores between 690 to 719 are considered good credit. Over 90% of lenders use FICO scores[2].

VantageScore was introduced in 2006 and uses a similar method by grouping a person’s credit information into six categories whereas FICO uses five. They also differ in their number ranges, the length of credit history required, the types of credit inquiries a person has made and the trending data a person may have developed over time.

What is a credit reporting agency?

A credit reporting agency or bureau is responsible for collecting and distributing credit information, which when compiled, creates a person’s credit score.

There are three major credit reporting agencies in the United States who lenders may choose to work with, Equifax, Experian and TransUnion, colloquially known as ‘The Big Three’.

Equifax Credit Bureau

Equifax is one of the largest credit reporting agencies in the U.S, with credit data from hundreds of millions of consumers and tens of millions of businesses worldwide[4]. You can order a copy of your credit report for free in 10 days if you haven’t ordered one in the previous year.

Experian Credit Bureau

While its roots may have started in Ireland back in 1996, Experian has since expanded all over the world. With access to extensive consumer and business data globally[5], Experian are experts in defining credit scores, so credit providers can make appropriate decisions regarding a customer’s request for credit.

TransUnion Credit Bureau

TransUnion has been around since 1968 and has since collected information on consumers and businesses across multiple countries[6]. By tapping into both credit and public data information, TransUnion provides lenders with expert information to help them make better informed decisions about credit applicants.

How to check your credit score?

There’s no hard and fast rule when it comes to checking your credit score, but you should be aiming to check in on your credit file at least once a year. While you can request a free copy of your credit history using one of the above credit reporting agencies, there are more familiar alternatives.

Outside of credit bureaus, you can access a copy of your credit file at:

How to Improve and Build Credit?

As you’ve probably gathered by now, your ability to access credit plays a big part in measuring your financial health. If you come to find your credit score isn’t up to scratch, don’t worry, your number isn’t set in stone. In fact, with a few easy tips and tricks, you can improve your credit score in no time!

Make Payments on Time

One easy way to improve your credit score is to make any upcoming payments on time, like your bills. This shows credit agencies you prioritize paying essential expenses and don’t attract late fees or interest. After all, nothing says financial responsibility like paid bills!

Optimize Credit Utilization

While it’s best to pay off your credit card balance in full every month to avoid interest charges, this isn’t feasible for every budget. In this case, aim to lower your card’s total balance to under 30% of the total credit limit[3]. From there, you can shoot for below 10% and eventually clear your balance completely.

Limit Your Credit Pulls

If you’ve been rejected on a credit application in the past because of your credit score, now is the time to stop making any more. Every time you submit a credit application to a provider, it is recorded on your file, regardless of whether it was approved or rejected.

Managing Cash Flow and Debts

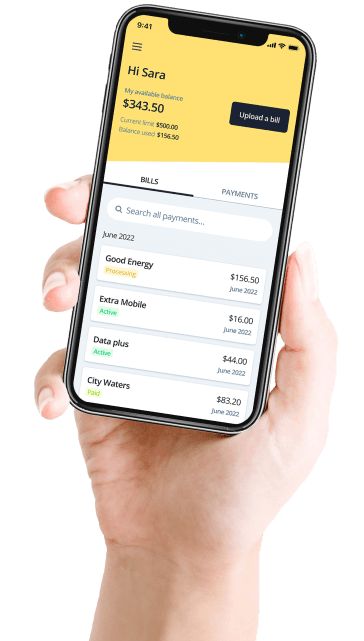

Our last tip for practising positive financial habits for a better credit score is to better manage your cash flow. Cutting back on certain spending might have felt like your only option to free up your budget in the past.

But thanks to the launch of new fintechs, like Deferit, you don’t have to sacrifice your lifestyle to stay on top of your finances.

Deferit is a budgeting app that splits bills into 4 installments, making them easier to manage. Deferit pays your biller upfront and on time, charges no interest and is full of flexibility, allowing users to reschedule payment dates for free. And with an app like Deferit on your side, you’ll have more space in your budget to pay off debt.

Want to give Deferit a try? Get started today and get your first bill paid with Deferit!

References

- myFICO. “What is a Credit Score?” myFICO Credit Education.

- myFICO. “FICO Scores - The Most Widely Used Credit Scores.” myFICO.

- Experian. “What Is a Credit Utilization Rate?” Experian Ask Experian Blog.

- Equifax. “About Equifax - Company Information.” Equifax Inc.

- Experian. “About Experian - Company Profile.” Experian PLC.

- TransUnion. “About TransUnion - Company Information.” TransUnion LLC.